About

This project will investigate – across countries and institutions – what characterises tax lawyers’ expertise, and how they draw boundaries between their own and other forms of expertise.

Who has power over tax policy?

Tax systems are shaped through professional practice by legal experts in the state apparatus and in the private sector, by those teaching tax law in universities and by those practicing in court.

This project will investigate – across countries and institutions – what characterises their expertise, how they draw boundaries between their own and other forms of expertise, and how the institutional context in which they practice underpin their definitions of legal expertise and authority.

Populist contestation of political, bureaucratic and expert elites has become a salient part of contemporary politics also in western democracies – as demonstrated by the Yellow Vests in France, Brexit, or by Trump’s followers in the US. There is a critique of unjust tax systems and these elites’ power to decide how the citizens’ money is spent.

Yet, do politicians really shape the tax systems? Surely, they are the ones who vote over them. However, legal experts are crucial in the process of shaping tax systems.

In the ministries of finance, they develop the legal texts on which the politicians vote, and when politicians bring them suggestions on new tax measures, the legal experts tell them what can and can’t be done – based on their expertise.

What is a good tax system?

But, wherein lies these legal experts’ authority to define what a good tax system is? And how does one really distinguish between legal expert judgement and political judgement in matters of tax? And do legal experts align with economic experts on tax issues, or do they represent a distinct voice?

Further, most of the limits to redistributive effects of tax systems are legal, with loopholes found with the help of legal experts in private firms counselling their clients. The clients are often multinational firms developing complex corporate structures constructed to contain legal ambiguities. The increasing internationalization of law and consultancy firms is accelerating this process, as well as new forms of professionalization among lawyers.

Primary and secondary objectives

The primary objective of this project is to develop a new theoretical and methodological framework to gain new knowledge on how legal professionals in tax law make claims to expert authority, and thereby fill gaps in sociology of professions, social studies of law and expertise studies.

The secondary objectives are:

- to describe the characteristics of legal expertise used in daily professional tax law practice (in policy making in ministries, in counselling on tax planning, in universities and in prosecuting or defense in court), and how it is distinct from adjacent fields of expertise

- to understand the way expertise in tax law is related to its institutional context (e.g. the organizations, sectors or countries they take place in and the cultural, normative and regulative elements in these social structures), and

- to advance theories on legal expertise’s sources of authority and legitimacy.

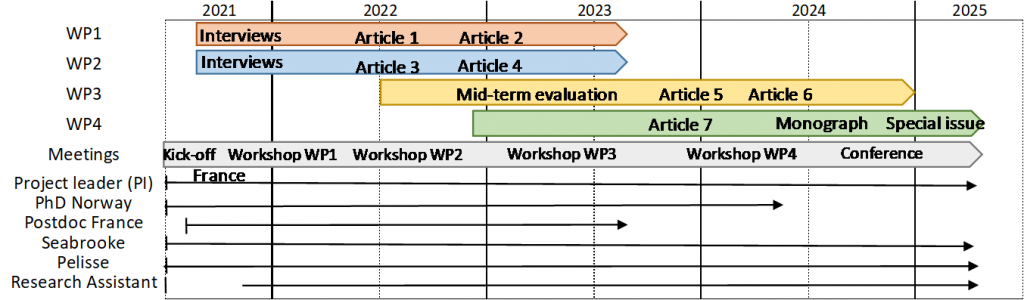

Timeline

General information

Project period: 01/04/2021-31/03/2025

Financing: The Research Council of Norway

Project number: 314825

Project owner: Centre for the Study of Professions (oslomet.no)